Here’s How Much House You Can Afford Under Canada’s New Mortgage Rules

The mortgage stress test is a tool used to ensure that buyers do not spend more on a home than they can actually afford.

By Sonia Bell and Wayne Karl

It’s January 2018, prospective homebuyers, and you know what that means: The new mortgage stress test is in play.

But what you may not know is how much it’s going to impact your homebuying budget. Nor would you be alone: A new study from ReMax estimates that 37 per cent of Canadians aren’t aware of how the changes will affect their ability to purchase a property in the future.

WAVEBREAKMEDIA VIA GETTY IMAGES

WAVEBREAKMEDIA VIA GETTY IMAGESIf you’re among them, you may be feeling the stress, indeed. But here’s our guide showcasing what you can afford with the new regulations.

Towards the end of 2017, the Office of the Superintendent of Financial Institutions (OSFI) introduced new, tighter mortgage rules, requiring borrowers with uninsured mortgages (those putting a down payment of 20 per cent or more) to undergo a stress test. As of Jan. 1, 2018, uninsured borrowers must now qualify at a new minimum rate — the greater of the Bank of Canada’s five-year benchmark rate, which currently sits at 4.99 per cent, or 200 basis points higher than their mortgage rate.

While the stress test aims at ensuring that borrowers can afford mortgage rate hikes, some sources are questioning — if not outright opposing — the latest mortgage rule.

“Those of us working in the mortgage industry question if now is an appropriate time to introduce more regulations, which will cool markets across the country further,” says James Laird, co-founder, ratehub.ca, and president of CanWise Financial. “We have yet to see the full impact of regulations added over the last 12 months, combined with rising interest rates. A more prudent approach would be to let these new variables work their way through the real estate markets and decide if further tightening is required.”

Natural supply and demand forces will always triumph over regulatory tinkering.Phil Soper, Royal LePage

Phil Soper, president and CEO, Royal LePage, is also wary of the new policy change. “It is prudent that policy makers introduce measures that help protect the housing market from runaway price inflation,” says Soper. “However, natural supply and demand forces will always triumph over regulatory tinkering. Attempting to use public policy to steer property prices in huge, rapidly growing cities like Toronto and Vancouver is like a tugboat trying to turn an ocean liner. Consistent, measured policy can have a positive impact. Just don’t try to turn the market on a dime or you risk sinking the ship.”

Importantly, prospective homebuyers, those who stand to be most affected, haven’t yet grasped the full repercussions of the new policy, which could disqualify 10 per cent of purchasers, according to The Bank of Canada.

Fifty-eight per cent of ReMax’s survey respondents are aware of the new rules, but 27 per cent of respondents stated they don’t believe it will impact the type of property they purchase; 18 per cent believe it will impact the property type they purchase; and 13 per cent are unsure of how the new regulations will affect their ability to purchase a property.

Homebuyers are purchasing in a rising interest rate environment — interest rates grew twice in 2017 and are expecting to continue to rise between 2018 and 2019, according to CMHC. The new stress test is aimed at protecting homebuyers; it is a tool used to ensure that buyers do not spend more on a home than they can actually afford and safeguards them from feeling financial stress should interest rates rise.

More Canadian real estate info from NextHome:

Royal LePage is among those to predict the new mortgage stress test will significantly influence the market, especially in the first six months of the year, as buyers re-evaluate their finances and expectations and adopt a “wait and see” approach. By reducing buyers’ purchasing power, the stress test will likely result in further demand for entry-level properties, namely the condominium segment, which could continue to drive prices higher, which could further limit what kind of property you can afford.

So, how much can you really afford?

The harsh reality is that the new rules will reduce homebuyers’ purchasing power substantially. In some cases, decreasing the overall price of a home they can afford by tens of thousands of dollars. We calculated how much a buyer can afford, now that the new rule has taken effect.

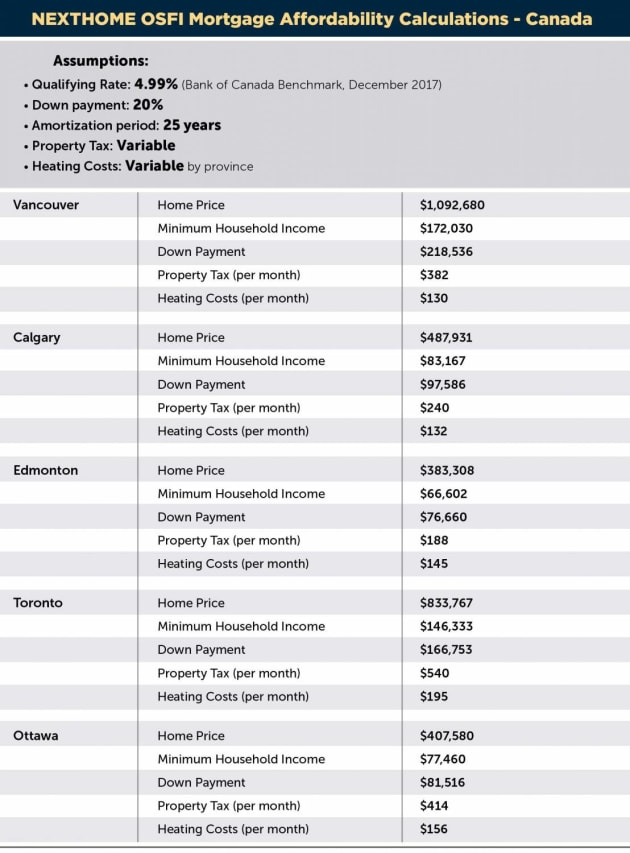

The methodology: Using ratehub.ca’s mortgage affordability calculator, we determined how much a family can afford with a household income of $100,000 and qualifying for a five-year fixed mortgage amortized over 25 years.

The corresponding chart presents a typical scenario: A family qualifying for a mortgage rate of 2.84 per cent. In this case, they would need to qualify at the Bank of Canada’s five-year benchmark rate, currently at 4.99 per cent.

We show the minimum household income required, and how much of a down payment you would need, in order to buy a home at the average price in that market.

Your guide to what you can buy:

SOURCE: RATEHUB.CA